Loan Scams: How to Find Out How Many Loans and Credit Cards Are Active in Your Name

Over the past few years, cybercrime has become a fast-emerging problem in the country. Nowadays, many people take loans or issue credit cards to someone without their knowledge. And to avoid such frauds, you must safeguard yourselves.

The fraud cases have increased in the digital era. In this regard, the government takes many steps to prevent such frauds. By the time the person comes to know about this loan, it’s too late.

Today, we are going to see how you can get such information of whether a loan has been taken or a credit card issued in your name or not.

Did you know that in 2021 alone, over 45,000 cases of loan fraud were reported in India, amounting to nearly ₹4.92 trillion? As cybercrime continues to rise, protecting your financial identity has never been more crucial.

How much loan or credit card debt is in your name?

You can easily know how many loans or credit cards are issued in your name by checking your credit report. Your CIBIL score will show how many loans or credit cards you have associated with your name, so it’s very easy to check.

For free, you can check your CIBIL score on several apps like CIBIL.com, Paytm, Google Pay, etc.

How to Check Your CIBIL Score: Get to Know

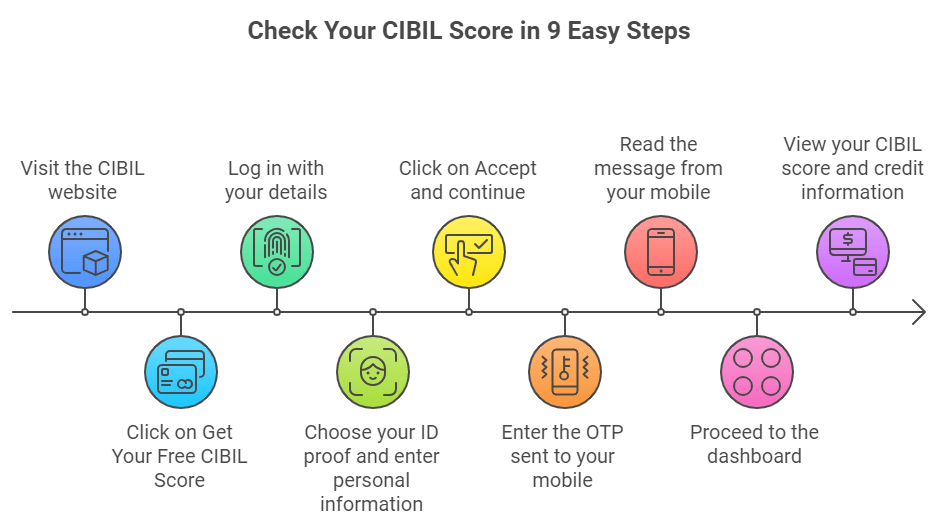

Step 1: Check out your CIBIL score here www.cibil.com

Step 2: From the home page, click on “Get Your Free CIBIL Score.

Step 3: Log in by filling in name, email ID, and password.

Step 4: After the login process, you have to choose your ID proof, enter your PIN code, date of birth, and mobile number.

Step 5: Once you have filled all this, click on “Accept and continue.”

Step 6: Now, OTP will be sent in your registered mobile number. So, enter that one.

Step 7: After entering that OTP, you will get a massage from your mobile.

Step 8: Then proceed further to the dashboard.

Step 9: Here, your CIBIL score will appear and you can also see how many loans or credit cards are issued in your name.

Also Read: [https://settlemyloan.in/everything-know-loan-settlement-loan-provider/]

Implications of Wrong Loans and Credit Card Entries on Your CIBIL Report

Having wrong loans or credit cards on your CIBIL report can cause problems like:

- Lower CIBIL Score: This makes it harder to get loans or credit at good rates.

- Loan Application Rejections: A low CIBIL score can lead to loan rejections or higher interest rates.

- Unexpected Financial Burden: Fake loans may result in surprise EMIs or collection calls.

- Legal Problems: If the fraud is not fixed, it could lead to legal action against you.

- Damage to Creditworthiness: Incorrect entries may stop you from getting loans or credit in the future.

Over the past few years, cybercrime has become a fast-emerging problem in the country. Nowadays, many people take loans or issue credit cards to someone without their knowledge. And to avoid such frauds, you must safeguard yourselves.

The fraud cases have increased in the digital era. In this regard, the government takes many steps to prevent such frauds. By the time the person comes to know about this loan, it’s too late.

Today, we are going to see how you can get such information of whether a loan has been taken or a credit card issued in your name or not.

Did you know that in 2021 alone, over 45,000 cases of loan fraud were reported in India, amounting to nearly ₹4.92 trillion? As cybercrime continues to rise, protecting your financial identity has never been more crucial.

What to Do if There is Fraud

If you detect an irregularity in your CIBIL score, then immediately contact the credit bureau and lender asking them to rectify it as quickly as possible.

Conclusion

In today’s digital world, safeguarding your financial identity is essential. With loan scams on the rise, being proactive about monitoring your credit report can help you detect unauthorized activities early. By regularly checking your CIBIL score and understanding how to manage your financial information, you can protect yourself from falling victim to fraud. Remember, knowledge is power—stay informed and take action to secure your financial future.

Do Like and Share

Do Like and Share