Understanding the Challenges of Missed EMI Payments and Debt Recovery Processes

The world of finance is a complex and challenging domain that requires diligent management. Whether juggling multiple loan payments or other financial obligations, your life is directly linked to numerous financial responsibilities. Falling behind on payments and slipping into debt is not only a difficult situation, but it can also lead to dealing with debt collectors and loan recovery agents, which can be overwhelming and stressful. However, stay hopeful! We are here to help you navigate this situation with confidence.

This guide underscores the severe consequences of missing Equated Monthly Installment (EMI) payments. Additionally, it will offer a comprehensive insight into debt collection procedures, outlining anticipated creditor actions and providing preparation strategies for borrowers. This will equip you with the knowledge to avoid calls and harassment from loan recovery agents. Stay informed and in control of your finances with our expert guidance.

What Happens When You Fail to or Cannot Pay

As a borrower, if you fail to repay the EMI on your loan/loans, financial institutions and banks begin the complex process of recovering their money. It begins with call center agents making calls to your number. If these are not answered, they are followed, by you as the borrower, receiving a formal legal notice.

This notice informs you of the money you owe, with a firm but polite message for prompt repayment. Many loan agreements also have arbitration clauses, which offer a way to settle disagreements through different means that help avoid lengthy court battles. Given below are some of the aspects that affect you as the borrower:

Lower Credit Score

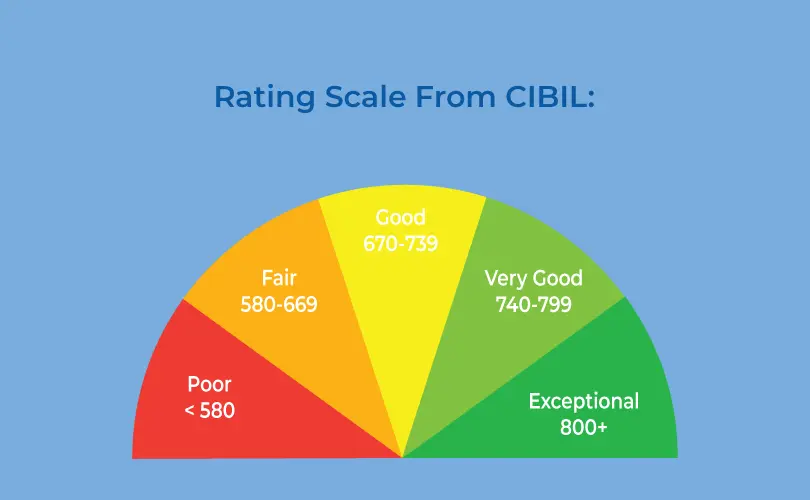

Your credit score is a numeric description of a person’s credit standing/creditworthiness/. This standing is calculated and attributed to a person depending on their debt amount, payment track record, and credit history. If all these are regular and timely, your credit score will be high.

Credit ratings are determined by credit bureaus like CIBIL or Credit Information Bureau (India) Limited, with other notable agencies including Equifax, Experian, CRIF High Mark, Credit Rating Information Services of India Ltd, Investment Information and Credit Rating Agency of India (ICRA) Ltd, Credit Analysis and Research (CARE) Ltd, and Acuite Ratings & Research Ltd.

This is the rating scale from CIBIL:

When an EMI payment is missed, for whatever reason, it becomes an adverse remark on your credit report. This leads to a reduction in your credit score and depending on the default and your overall credit history, your credit score can fall from 50 to 100 points.

This slight fall would reflect poorly and affect your credit rating. A lower credit rating would make it harder to secure loans, get a credit card, or even buy high-worth items on EMI. Even if you do manage to get a loan, it would be at higher interest rates and charges.

Repossession of Collateral

In the unfortunate event that you are unable to pay your loan, the lender is authorized to take control of the collateral and sell/auction it off to recover the loan amount. A loan against a collateral – a collateral is an asset that is used as ‘security’ to ensure the repayment of the loan. Such a situation proves to be highly embarrassing and stressful for the borrower, especially due to societal pressures and fear of ridicule.

Litigation Process

In the case of repeated non-payment of EMI installments, and where there is no collateral, the lending body could initiate legal action against you. This ‘action’ could be in the form of a court case/lawsuit or enforcing wage garnishment (Wage garnishment means that a part of your paycheck is taken directly by your employer to pay off the money you owe.

This happens when a court orders it because you haven’t been able to pay your debts through other means. It’s a way for them to get their money back). This too can be highly stressful given the social stigma and embarrassment. As mentioned above, if you can preempt that you will not be able to pay your installments, connect with the lender immediately. They could help to find an easier and more feasible way to make these payments.

Things To Do If You Default

If you do miss an EMI payment, it is necessary to take prompt measures to amend your credit score. Inform your creditor immediately, and make future payments on time, or ask to extend the duration of your loan payment. When you inform your creditors, they will be able to help you and will know that you are not trying to defraud them. Here are a few steps to help you:

Put together a realistic budget

Create a budget that is realistic but eliminates all avoidable and extraneous expenses. Keep only things that you need, such that you can easily pay off your EMIs and save yourself from stress and embarrassment.

Promptly inform the Lender

Always inform the lender in advance – share the reasons for your inability to pay and show them any documents of previous regular loan repayments. This could help to get more time to pay or reduce the amount of each EMI installment. You could alternatively seek a moratorium or deferment of your payment. You would, however, incur a late payment fee for such a request. Your lender could restructure your loan to get a tenure extension as well – especially in the event of losing a job or some other unexpected financial loss. State your request in writing, mentioning the period for which you seek the extension, and confirm that all your payments will be on time thereafter.

Liquidating Assets or Investments

In case you have made some investments or have some assets that you can liquidate, this will help you gain relief from any outstanding/late payments on your loan. This will save you from a higher rate of interest and the penalty charge for the overdue amount.

Financial Support from Family and Friends

If possible, lean on your family and friends for financial support. This may not be ideal, but at least you will not have to face harassment from recovery agents nor accumulate a bigger financial liability in the form of late charges, nor face legal punitive action.

Settle your Loan

If you can raise a lump sum amount, speak with your lender to check if you can pay off the loan as a settlement. This means no further payments, and you would be free from debt. However, a settlement also affects your credit score quite adversely.

What Are Your Rights Even As a Debtor

Running into unexpected financial difficulties is extremely stressful, even without the added consequences mentioned above. However, even as a borrower you have certain rights and are protected. Given below are some of the rights:

- Lenders must notify you of missed installment payments, allowing you to settle dues after receiving adequate notice.

- Borrowers have the right to specify preferred contact times for lenders, with restrictions on contacting before 7 am and after 7 pm.

- Personal information and loan details must be kept confidential by lenders, who are also barred from abusive behavior.

- Borrowers can determine the value of collateralized assets during repossession proceedings.

- Borrowers are entitled to accurate information about loan recovery agents contacting them.

- In cases of harassment from recovery agents, borrowers can file complaints with regulatory bodies and engage legal assistance.

As a borrower facing financial turmoil, you do not need to undergo more stress in the form of recovery agent harassment. It is imperative to know your rights and undertake the necessary action against the harassment. By taking these actions you save yourself from harassment and ensure the recovery agency/agent is liable for the misdemeanour.

Finally

In summary, it’s important to understand the significance of missing EMI payments, as it can have a lasting impact on your financial standing. Avoiding actions that could harm your credit score is crucial, as rebuilding it is a gradual journey. While making consistent and timely payments is vital, repairing your credit takes time and patience. Typically, it may take around six months to start seeing improvements and achieving a desirable score could take up to two years. Since your credit history reflects years of financial behavior, maintaining it is essential. Therefore, it’s important to understand your financial responsibilities and prioritize actions that support your long-term financial well-being.

We at Settle My Loan can help you gain peace of mind. Our personalized solutions are designed to meet your needs directly. Begin your path to stability and empowerment today. Get in touch with Settle My Loan, and let’s work together to overcome your financial challenges.

What will happen if I have stopped paying EMI for a personal loan and credit card bill due to job loss from the past 3 months?

Suppose you ceased paying EMIs after three months because you lost a job, chances are your accounts are Non-Performing Assets (NPAs) at the bank, and this will be disastrous to your CIBIL score. You will have to contend with increasing late payment charges, penalty interest as well as unending calls by recovery agents. The lender can take legal action in order to collect the debt and in the cast of the credit cards, your credit limit may be decreased or the card may be cancelled. It is paramount that steps are taken proactively to ensure that there are no further consequences.

FAQ

Do Like and Share